(Schiff)—The technical position for gold is looking very positive for higher prices. But technical analysis should be backed by fundamentals.

To a large extent, fundamentals are in the eye of the beholder, whose opinions in any situation can vary from positive to negative and everything in between. But even for the economic optimists, there are gathering clouds on the horizon likely to continue undermining the global economic outlook, the dollar, and all financial asset values. Fiat currencies are being downgraded relative to real money, which is gold.

Current thinking is that inflation is a diminishing problem and that the interest rate spike is over. In this article, I point out where inflation expectations err and the mistake of believing that interest rate control is the solution.

It follows therefore that G7 debt traps are a more serious problem than generally realized. Furthermore, China and Russia are aware of the likely impact of current events on G7 currencies, and this is why they have accumulated hidden gold reserves.

In short, we face a transition between failing fiat and emerging gold-backed currencies, which might explain why gold’s technical position looks so positive.

If you are a chartist, you will judge the current market position for gold to look very bullish. The closely followed moving averages in the chart above are in a bullish sequence, both rising and the 55-day turning sharply higher. The current decline in the gold price should find strong support at its current level, which is between $1910—$1923. A follower of Elliot Wave Theory might say the most likely interpretation is there was a three-leg flat consolidation commencing in August 2020, completing in November 2022, lasting slightly more than 13 months which is a Fibonacci number. The subsequent move is the start of a new bull market.

Despite the backward-looking nature of technical analysis, the bullish argument is compelling, particularly in the context of heightened tensions in the Middle East and a looming global recession. The plain fact is that going into a recession we see G7 government finances (with the sole exception of Germany’s) already mired in debt traps, likely to lead to a series of funding crises. These funding crises inevitably drive up bond yields and divert investment capital from private sector actors to government debt, worsening the economic outlook. And since government revenue depends on profitable economic activity, the funding squeeze ends up undermining government finances.

It is a situation that echoes the 1970s when currency instability led to gold rising from the previously established Bretton Woods level of $35 to $850 on 21 January 1980. At the same time, the Federal Funds Effective Rate rose from a low of 3.3% in February 1972 to a high of 13.8% when gold peaked, going on to over 19% the following year. Today, the idea that both gold and interest rates can rise together is dismissed by the banking and investment establishment. Yet, since August 2020 the Fed Funds Effective Rate has risen from the zero bound to 5.33% currently and gold priced in dollars is roughly unchanged — hardly the negative correlation upheld by the establishment.

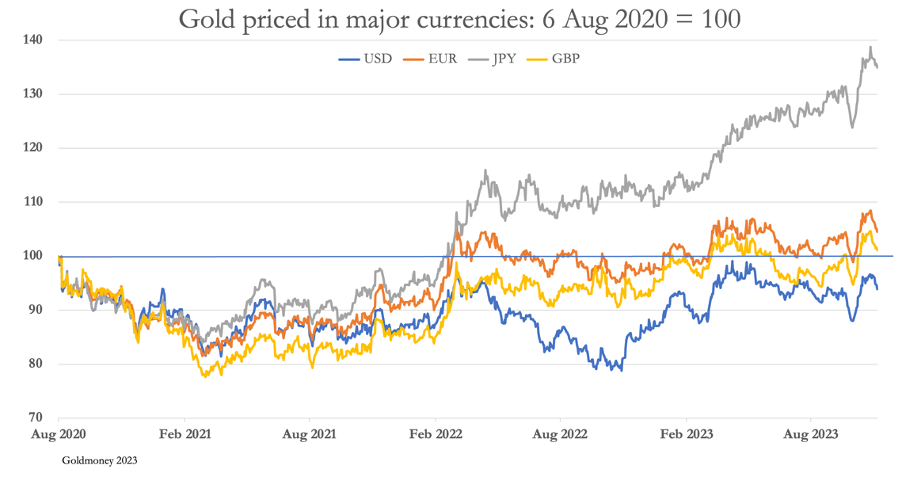

Due to the dollar’s relative strength, priced in other currencies, gold is now higher than it was when it first peaked on 6 August 2020, illustrated in the chart below.

In the case of Japan’s yen, it is 35% higher, 4% higher in euros, and 1% higher in sterling while in dollars it is 6% lower. The yen has been particularly weak, due to the Bank of Japan’s monetary policy keeping its deposit rate negative.

With it being widely recognized that the global economy faces an economic downturn, there is also a misconception about the consequences for consumer prices. It is assumed that a recession reduces demand leading to a glut of goods and therefore lower prices. That being the case, they say that with their improving purchasing power currencies might be expected to strengthen against gold. This misconception dates back to the early 1930s when goods were effectively priced in gold because the dollar was tied to it at $20.67 to the ounce. The fact that the dollar was devalued 40% by President Roosevelt in 1934 confirms that the monetary strength was in gold, not the dollar currency. And in the 1970s when the dollar and all other currencies were detached from gold, recessions were accompanied by escalating rates of consumer price inflation.

These and other issues need to be addressed in order to understand why the gold chart looks so positive, and what that implies.

Why consumer prices fell in the Depression

As mentioned above, the experience of the early 1930s was of a significant decline in consumer prices. Between December 1929 and June 1932, the consumer price all items index is estimated to have declined by 8.3%, with food worst hit, down 13%. This echoed the fall in the general level of prices in the 1920—1922 slump when the CPI declined by 9.7%.

Based on this experience, economists in the late 1930s concluded that in a recession prices would always decline and that Say’s Law, which was the basis of classical economics was incorrect. Certainly, there are items that appear to escape the strictures of Say’s Law, such as commodity and raw material prices which experience a decline in demand in a slump. But even that assumes commodity outputs are not curtailed in response to falling demand, which Usually is not the case. Essentially, mismatches between supply and demand are just a timing issue.

In both the early 1920s and early 1930s depressions, food prices were further undermined by the rapid mechanization of farming which boosted output. But as was the case in the 1920—1922 slump, the economic difficulties of the early 1930s were the washing out of excess credit generated in the previous credit boom.

The point about Say’s Law is that it posits that we produce to consume. Therefore, there cannot be a general slump because production will decline with consumption. One can go further, and state that apart from destocking (which today with just-in-time inventory management has been minimized) employees will lose their employment first before they reduce their consumption.

In his desire to promote statist intervention, Keynes had to dismiss Say’s Law which he did on spurious grounds:

“Thus, Say’s Law that the aggregate demand price of output as a whole is equal to its aggregate supply price for all volumes of output, is equivalent to the proposition that there is no obstacle to full employment. If, however, this is not the true law relating the aggregate demand and supply functions, there is a vitally important chapter of economic theory which remains to be written and without which all discussions concerning the volume of aggregate employment are futile.”

This is a wilful misrepresentation of an obvious truth that was never intended to be more than a generalization, and certainly not to be justified in a mathematical equation which is effectively Keynes’s argument. But today, Keynes’s General Theory is the vade mecum for mathematical economists and misleads them about the relationship between a slump in business activity and prices.

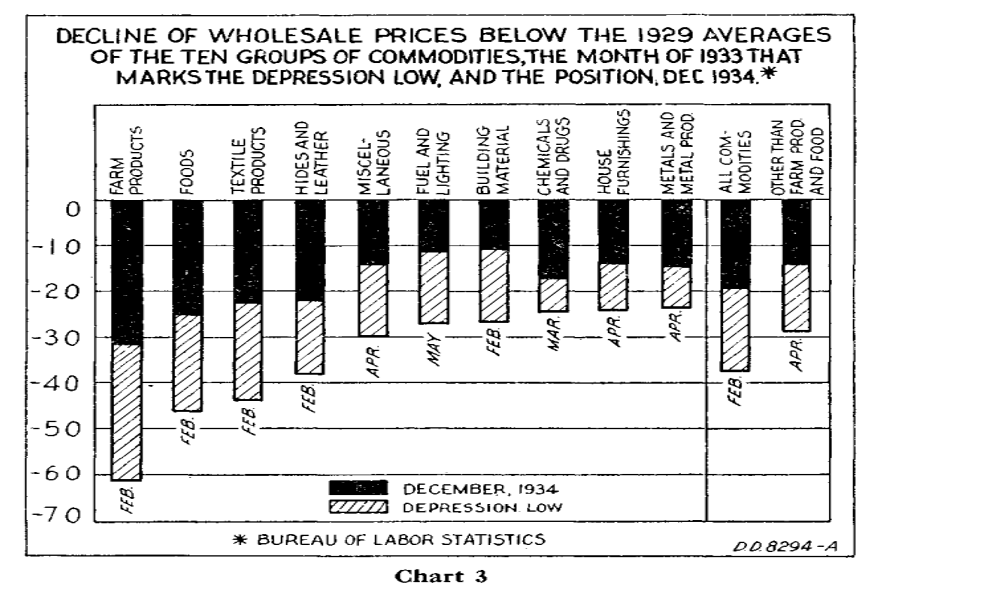

As we saw in the early-1930s, prices did fall by 8%. Commodity prices for farm products declined by 60% between 1929 and February 1933, which compares with the decline of food prices in the CPI of 13%, indicating that food production costs actually rose offsetting most of the decline in product values to farmers. The reasons for these declines are explained more fully below.

The February 1935 Survey of Current Business on wholesale commodity prices also noted the following:

“Another classification of the Bureau of Labor Statistics series is given in chart 3 [reproduced below], showing the 10 commodity groups arranged according to the degree of decline in the different groups. As shown therein, the prices of three groups, metals and metal products, house furnishings, and chemicals and drugs, declined slightly less than 25 percent from 1929 to the lows which were reached in the early part of 1933, and the prices of building materials only a little more than 25 percent.”

Yes, these are declines in the general price level, but not as severe as we have been led to suppose today. And they can be easily explained without denying Say’s Law. In 1929—1932 there was the stock market crash, a series of regional banking panics in 1931 and 1932, and in March 1933 the commercial banking system more or less collapsed. Demand deposits contracted by 35% between 1929—1933. In all, some 9,000 banks failed and there was no deposit insurance.

At that time, the dollar was freely exchangeable for gold, so the contraction of credit in the economy had the price effect of a sudden and widespread scarcity of gold. Clearly, it was this scarcity that drove prices lower. Furthermore, allowing for deposit contraction amounting to 35%, non-food commodities in the chart above on average didn’t fall at all (see the last column — “Other than farm products and food”).

The position today is completely different. Currencies are no longer tied to gold and are freely inflated by central banks when deemed necessary. Bank credit is contracting, but the quantities so far are minor. In the event of bank failures, there are deposit guarantees and we can be certain that rather than fail, banks will almost always be rescued by their respective authorities.

In short, there is no certainty over the future purchasing power of today’s fiat currencies. But we are getting to the nub of why the general level of prices will rise in the looming recession: if anything, the future expansion of central bank credit to offset a recession, potential bank failures, and the inevitable unwinding of malinvestments are together set to dilute the purchasing power of all G7 currencies, even to the point where the public’s faith in them becomes undermined.

This brings us to the role of interest rates in the context of currencies. As we saw in 1981, Fed Funds Rates of over 19% ended the bull market run in gold and led to a long decline in dollar interest rates. It worked because foreigners saw a positive return at those rates after allowing for the anticipated loss of future purchasing power in dollars. They will make the same judgment today, only their holdings of dollars and dollar assets in the US financial system at $33 trillion are even greater than the US GDP. To this must be added offshore dollar credit estimated by the Bank for International Settlements at a further $85 trillion, and a further $10 trillion for Eurobonds. Prospective instability in the dollar’s purchasing power could easily lead to unrestrained foreign liquidation of these massive quantities.

There can only be one conclusion: despite the current optimism in financial markets, prices will continue to rise at far above the central banks’ mandated rate of 2% and interest rates will rise with them. And if the 1970s does turn out to be a precedent for the 2020s, we can expect far higher interest rates in the coming years.

The futility of economic management by interest rates

In an attempt to stave off inflation, central banks jacked up interest rates, destroying all government, banking, and business models. The problems caused are obvious to everyone down to the lowly householder facing higher mortgage payments and credit card debt. Naturally, there is a backlash with mechanical monetarists and others saying that the authorities have gone too far. In their search for price stability, mainstream economists are now trying to determine the natural rate of interest, which today they term r*. It will be no surprise that the answer they come up with is that it should be lower.

The concept originates with the analysis of Knut Wicksell, who in 1998 explained that a natural rate of interest represented the rate of interest on loans that equilibrate with respect to commodity prices, neither raising nor lowering them. His conclusions came at a time when gold standards were ubiquitous, and applied to monetary systems where credit in the form of currencies was regarded credibly as gold substitutes.

It should be noted that the concept did not apply to the purchasing power of gold solely, which was determined as a fully objective international average, but to credit redeemable in gold plus interest in a national context. It was the nationally determined rate of interest redeemable in gold that made the difference between the value of gold in one center versus another, arbitrage ensuring that prices did not stray significantly from their international norm.

As noted above, Wicksell’s proposition was made at a time of universal gold standards. He described the natural rate of interest required to bring the domestic relationship between gold and commodities in line with the international average value of gold’s purchasing power. However, the situation with unstable fiat currencies is entirely different, a fact that is ignored by economists who believe that fiat currency relationships with commodities are no different from that of gold.

But r* is entirely theoretical and cannot be defined. For this reason, even Fed officials disagree, with the New York Fed estimating it at 1.13%, and the Richmond Fed at 2.2%. But all this fiddling with theoretical numbers, as was the case with the closely associated Taylor Rule is irrelevant and flies in the face of empirical evidence. Even before Wicksell, the use of interest rates to stabilise demand for commodities, which we can also imply extends to other production inputs, led to enormous problems. The management of interest rates was always aimed at the wrong objective. An illustration of this important point is called for.

In 1799, there was a financial crisis in Hamburg which drove the discount rate there to 15% (equivalent to an interest rate of over 17.5%), attracting gold away from the Bank of England. This was because traders could redeem sterling for gold at the Bank giving up an interest return on sterling of just a few percent and ship it to Hamburg where it would earn an extra return because of the discount. After the perils and costs of shipping, a trader would make a clear profit of over ten percent — redeemable in gold.

At the time, this arbitrage was little understood by the authorities framing banking law, and they made the same mistake in the 1844 Bank Charter Act. Consequently, there were three failures in 1847, 1857, and 1866 when the Bank of England had to suspend its gold exchange obligations under its charter. The root of all these failures, including the run on gold reserves in 1799, was that the Bank was managing interest rates with an eye to economic factors and not the level of monetary reserves. In the conflict objectives of interest rate setting between satisfying currency and domestic economic stability, the wrong choice was always made.

Today, gold reserves are not involved, replaced by an unstable currency regime. This leads the authorities into a further dilemma: should each central bank use interest rates to stabilise their currencies against the dollar, or should they use them to stabilize their currencies against commodities as Wicksellian theory demands? Clearly, they are beholden to following the dollar. And if the dollar is the replacement for the barbarous relic, surely the interest rate objective for the dollar must be one that equilibrates with respect to commodity prices, neither raising nor lowering them.

Survival Beef on sale now. Freeze dried Ribeye, NY Strip, and Premium beef cubes. Promo code “jdr” at checkout for 25% off! Prepper All-Naturals

You would think that by focusing on consumer prices it is indeed the Fed’s interest rate objective. Debating Wicksellian theories and r* assumes that dollars are the new gold and that while other currencies should manage their interest rates with a view to their dollar exchange rates instead, the Fed’s objective is to achieve that Wicksellian stability. But this leaves the Fed with the problem that no one can agree on what the theoretical r* should be, let alone what it should be in the future. And no one in the monetary and credit establishment appears to understand that Wicksell’s theory was between one commodity which happens to be universally accepted as physical money without counterparty risk in a domestic context and all other commodities. This is not the same as the relationship between commodities generally and detached credit, which is what a fiat currency represents, whose future value is not tied to commodities at all but to the market’s faith in future monetary and fiscal policies.

Under a gold standard and without central bank intervention, undoubtedly Wicksellian theory makes sense. But even then, the situation is dynamic, with events elsewhere influencing interest rate outcomes as the 1799 experience with Hamburg illustrated. r* as a concept can only be set by markets and events, and this is even truer in the case of unstable fiat currencies, whose value with respect to gold and therefore the general value of commodities is completely subjective. If one was to guess at the current dollar r* it would be over 4.5% (the current yield on the 10-year US treasury benchmark), not the 1.13% guess by the New York Fed. Instead, Fed officials optimistically take forward interest rate expectations as their basis for determining r*, which they themselves set by indicating their future interest rate expectations.

Consequently, we can see that the mistakes in US credit policies with respect to the dollar’s own future are at the most fundamental level. And because all other currencies are dependent on the dollar for their relative values, they are tied to the dollar’s ultimate failure. And it’s not just US monetary policy: the prospect of soaring US fiscal deficits debasing the dollar transmits into the debasement of all the other currencies as well.

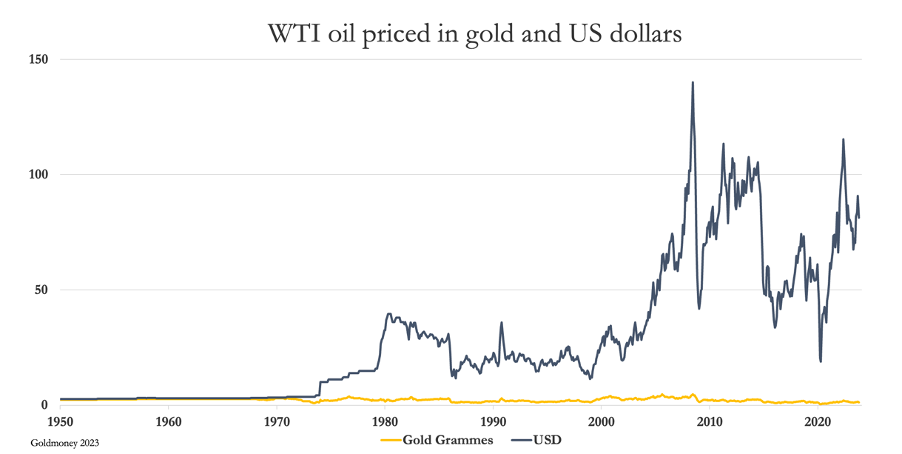

Even to this day, the relationship between gold and commodities has remained stable, as the chart below of the most fundamental unit of energy, oil, priced in both dollars and gold clearly demonstrates. This is not true of the dollar.

I have run similar charts in other commodities and found the same applies. Combined with the erosion of the dollar’s purchasing power since the Bretton Woods Agreement was suspended in 1971, we can see that it is gold that retains its international role as money and not the dollar, whose purchasing power is both volatile and rapidly eroding. It is a submission to statist propaganda for economists to maintain that gold is no longer money, replaced by the dollar.

The mistaken approach to interest rates by the US monetary authorities, together with the US Government’s soaring fiscal deficits confirms the technical conclusion of the headline chart to this article: that the dollar and all other fiat currencies’ purchasing power will continue to decline, reflected in higher prices measured in them for gold.

Funding budget deficits

One of the problems encountered in the 1970s was the reluctance of foreigners to fund government budget deficits at low interest rates. This hit the UK particularly hard, where a left-wing government was committed to destroying personal wealth and running budget deficits.

At that time the US was in a far better position. Between 1971 and 1980, the sum of budget deficits for the US Government over the ten years was $421,823 million, 15% of 1980’s GDP. By way of contrast, the total budget deficit for the last ten years totaled $12,918 billion, 47% of 2023 GDP. Furthermore, US debt to GDP in 1970 was 34%, while today it is 122%. That is the difficult starting point for US deficits going into a recession. With continual and accelerating deficit financing in prospect, the question arises as to what level will the US’s debt to GDP ratio rise, and what will be the consequences for the borrowing rates required to keep foreigners recycling dollar trade balances into US Treasuries when they are already heavily overexposed to dollar credit.

Out of the G7 countries, US government finances are not the worst. Japan heads the list at over 260% debt to GDP, followed by Italy at 144%. The Japanese position is particularly alarming in a global context. Currently, the government’s budget deficit at 6.4% of GDP is estimated at U37,250 billion. A one percent increase in average borrowing costs adds U15,000 billion to the deficit. It is hardly surprising that the Japanese strongly resist increasing bond yields, let alone because of the impact on the Bank of Japan’s balance sheet which owns an estimated 53% of all government bonds.

Japan’s putative financial crisis is important for the rest of the world, partly because Japanese institutions have invested in other markets in order to enhance returns, and partly because negative short-term rates are a highly attractive source of leveraged funding in other markets. So long as this situation persists, not only are there leveraged profits to be made between different treasury bill markets but there has been a substantial bonus from the yen’s decline. Consequently, on rising yen interest rates — which are now inevitable — not only will Japan be plunged into crisis, but it will lead to a significant contraction of global credit flows.

These aspects of G7 debt traps are just one side of the equation. It is not only soaring deficits driving debt-to-GDP relationships but the consequences for GDP itself. GDP is bolstered by government deficits as well as by changes in the level of outstanding commercial bank credit. These facts make GDP a badly corrupted indicator of economic activity, allowing government agencies to propagandize economic growth and conceal evidence of declining underlying economic activity. Other government statistics such as employment surveys are notoriously inaccurate, and one suspects are used to tell anything but the truth. But perhaps the best indicators are of logistics, and these tell us of multiple bankruptcies in the US trucking industry. A further indicator is US tax revenues, which have declined sharply since the peak in 2022’s Q2.

The consequences of many years of ultra-cheap borrowing costs followed by a substantial rise in interest rates cannot be denied. Not only have they thrown the entire banking system into a global crisis, not only have they sprung debt traps on high-spending governments, not only have they undermined personal and corporate wealth, but they have exposed massive industrial malinvestments on a global scale. Inevitably, the changed interest rate situation will continue to lead to bankruptcies and bank failures for years to come, many of which will demand state support for fear of a total collapse of the global credit system.

The unwinding of these distortions has become inevitable, leading to a credit contraction in the private sector, made worse by the demands of governments for yet more credit. This redeployment of credit from genuine economic activity to government finances worsens the situation by compromising government revenues even more. Declining tax revenues contribute to soaring deficits. This increasing shift of economic resources to the financing of runaway government deficits is bound to come at the expense of fiat currency dilution and yet higher bond yields.

Unless it can be stopped, a total collapse of the fiat currency credit system will be the end result. The only solution is to tie credit credibly to gold, making credit exchangeable for bullion and coin on demand. But how can this be achieved by governments whose gold reserves are depleted, and when perhaps as much as one-third of them are double counted so don’t exist? How can governments reverse a century of progressive intervention? How can the political class stop minding everyone’s business, when they are elected to do just that?

Undoubtedly, it was an early understanding of this increasingly inevitable endpoint that persuaded the Chinese and then the Russians to accumulate enough gold to protect themselves and their populations from the follies of G7 fiat currency management.

China, Russia, and BRICS+

Do not be misled by China’s official gold reserves. China has been accumulating gold since the Peoples Bank was appointed under China’s Regulations on the Control of Gold and Silver, dated 1 July 1983. For nineteen years, China accumulated gold during a prolonged bear market as Swiss banks and others gave up on gold and sold down bullion holdings for their customers. Western central banks reduced their holdings and leased gold into the market, never to return. Only when the Peoples Bank had accumulated enough gold that it finally rescinded the ban on personal ownership, opening the Shanghai Gold Exchange in 2002, subsequently advertising to encourage people to acquire gold. And in all that time, China invested heavily in mine production and refining capabilities, importing enormous quantities of bullion from the West and doré for refining. For forty years now, China has been a Hotel California for gold, with virtually no bullion leaving.

Why this obsession? Between hidden stocks and the private sector, I estimate that between the state and the people China could have accumulated over 50,000 tonnes, representing roughly 25% of all gold mined throughout history. This gold habit has spread beyond China to Asian partners in the Shanghai Cooperation Organisation. And belatedly, Russia began following the same course as China in the wake of sanctions imposed on it by the West in early 2022.

Russia tried to get a gold-backed trade settlement currency on the BRICS agenda at the Johannesburg summit last August. It was a move that appeared to have been supported by some nations, presumably frustrated at the devastating costs to their own economies of the lack of credibility in their own currencies and a desire to be paid for their exports in something better than other BRICS members’ currencies.

China and India were not so keen. The inscrutable Chinese take a long view, letting the Americans make all the monetary policy mistakes, from which they have ultimately protected themselves by accumulating a huge chunk of the world’s above-ground gold stocks. China does not wish to be blamed for destabilizing the dollar by being party to such a radical step as backing any official gold substitute currency. Furthermore, paying for commodity imports in her own fiat currency is preferable to her than paying in renminbi backed by gold.

India remains thoroughly Keynesian in its monetary policies, and her increase in gold reserves has been minor in the context of both her population and economy. The Indians are not fellow travelers. But Russia takes on the presidency of BRICS from January, so her proposals to incorporate gold into trade settlement will get another airing.

New BRICS members include Saudi Arabia and the United Arab Emirates who certainly prefer gold-related payments for their oil and gas exports to national fiat currencies. Interestingly, almost all the Shanghai Cooperation Organisation members, associates and dialog partners attended the Johannesburg BRICS summit, strongly suggesting that BRICS and the SCO will be merged.

That being the case, we can expect Iran and other oil and gas exporters to join. Russia’s case for a gold-backed trade settlement currency is likely to be advanced again. Furthermore, Russia herself would benefit enormously from backing the rouble with gold, allowing her to reduce interest rates from current crippling levels.

Not only has Russia accumulated the fifth largest official gold reserves at 2,330 tonnes, but she can mobilize bullion held in two state funds believed to total a further 10,000 tonnes. Furthermore, the lesson of how Hamburg drained the Bank of England of its gold in 1799 by interest rates being raised to 17.5% gives us (and the Russians with interest rates nearly at a similar level) a clue as to how to bolster her reserves on a gold standard even further, draining western capital markets of their physical liquidity.

Conclusion: the fundamentals for gold appear to fully support the technical case in our headline chart.

Subscribe for free to the America First Report newsletter.

- See https://www.bls.gov/opub/mlr/2014/article/one-hundred-years-of-price-change-the-consumer-price-index-and-the-american-inflation-experience.htm

- Ibid.

- See https://fraser.stlouisfed.org/files/docs/publications/SCB/pages/1935-1939/2755_1935-1939.pdf

Controlling Protein Is One of the Globalists’ Primary Goals

Between the globalists, corporate interests, and our own government, the food supply is being targeted from multiple angles. It isn’t just silly regulations and misguided subsidies driving natural foods away. Bird flu, sabotaged food processing plants, mysterious deaths of entire cattle herds, arson attacks, and an incessant push to make climate change the primary consideration for all things are combining for a perfect storm to exacerbate the ongoing food crisis.

The primary target is protein. Specifically, they’re going after beef as the environmental boogeyman. They want us eating vegetable-based proteins, lab-grown meat, or even bugs instead of anything that walked the pastures of America. This is why we launched a long-term storage prepper beef company that provides high-quality food that’s shelf-stable for up to 25-years.

At Prepper All-Naturals, we believe Americans should be eating real food today and into the future regardless of what the powers-that-be demand of us. We will never use lab-grown beef. We will never allow our cattle to be injected with mRNA vaccines. We will never bow to the draconian diktats of the climate change cult.

Visit Prepper All-Naturals and use promo code “veterans25” to get 25% off plus free shipping on Ribeye, NY Strip, Tenderloin, and other high-quality cuts of beef. It’s cooked sous vide, then freeze dried and packaged with no other ingredients, just beef. Stock up for the long haul today.