While it has been a relatively quiet week in the financial sector, it may not be long before the economy takes over headline news again.

ZeroHedge News reported today that U.S. banks are experiencing more runs on deposits.

US Bank Deposits Resume Outflows, Led By Large Institutions; Small Bank Loan Growth Slumped

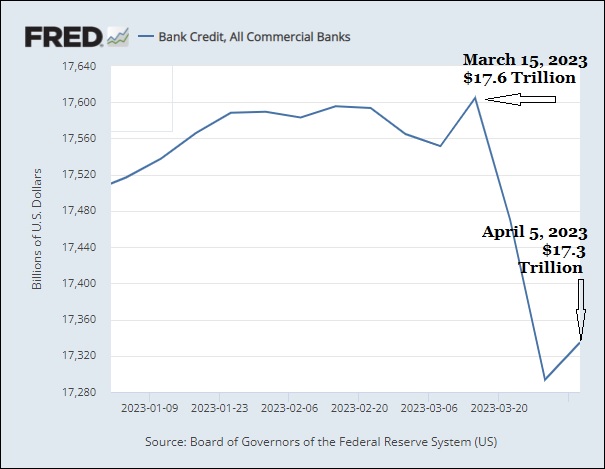

It’s late on a Friday afternoon, but there’s still more things to worry about as The Fed’s H.8 (commercial bank deposit data) just dropped.

After yesterday’s report showed the Fed balance sheet shrinking but bank bailout facility usage higher, US commercial bank deposits (ex-large time deposits) unexpectedly resumed their freefall (during the week-ending 4/12), tumbling $68.66 billion to the lowest since April 2021…

Pam Martens of Wall Street on Parade addressed the current “credit crunch” that was revealed this week with the release of the Federal Reserve’s “Beige Book” report.

Fed’s Beige Book: The Credit Crunch Has Arrived in New York, California and Texas

On Wednesday, the Federal Reserve released its Beige Book, a compilation of current economic conditions in each of its 12 Federal Reserve districts. The information that was collected in each of the regional reports was gathered on or before April 10 – so it is relatively current.

It is not a good sign that three of the Fed districts that pump out a significant chunk of U.S. GDP reported that bank credit had tightened noticeably, ostensibly as fallout from the banking collapses in March and depositor runs.

The New York Fed reported that credit conditions in the Second Fed District, which includes New York state, the 12 northern counties of New Jersey, Connecticut’s Fairfield County, Puerto Rico and the U.S. Virgin Islands, “deteriorated sharply.” It summarized the situation as follows:

“Conditions in the broad finance sector deteriorated sharply coinciding with recent stress in the banking sector. Small to medium-sized banks in the District reported widespread declines in loan demand across all loan segments. Credit standards tightened noticeably for all loan types, and loan spreads continued to narrow. Deposit [interest] rates moved higher. Finally, delinquency rates edged up on residential and commercial mortgages.”

Almost everyone now in the corporate news media financial sector is admitting that the U.S. Dollar’s decline is a foregone conclusion in the future.

The only question left is, how quickly will it collapse?

Alasdair Macleod of Goldmoney has written the best analysis of the current U.S. Dollar situation that I have read so far, and it was republished on ZeroHedge News as well.

This is a bit of a long read, but it is well worth it to understand what is probably in store for the U.S. Dollar in the future, as he tackles the question: “How quickly will the dollar collapse?”

If you want a spoiler statement from this article, it would be this:

Assuming that foreign holders reduce their dollar exposure and at the margin buy renminbi (Chinese currency), the fall in the dollar relative to the renminbi could be unexpectedly sudden and substantial.

How Quickly Will the Dollar Collapse?

This article looks at the factors behind the growing rejection of the dollar for trade settlement purposes by non-aligned nations around the world. They no longer fear political or economic reprisals from America.

The dollar’s monopoly was notably challenged by Saudi Arabia, which removed itself from the US’s sphere of influence to that of China and Russia. Consequently, peace has broken out throughout the Arab lands.

But rising interest rates have destabilised western banking systems, which have added to the attractions of payment in China’s renminbi relative to maintaining bank deposits and investments in the currencies of the western alliance — particularly of the dollar. Foreigners hold $7 trillion of deposits and short-term bills and $24.5 trillion in bonds and equities. These balances are becoming surplus to their needs.

The outlook is for US bank credit to contract further, which will drive interest rates even higher. More banks can be expected to fail. Foreigners are bound to become increasingly reluctant to hold dollars, which they will sell. Therefore, the question now is not how much will the dollar decline, but how rapidly.

Introduction

We know that the Russia and China’s desire to do away with the dollar is coming true, due to factors beyond their immediate control. Increasing numbers of nations are now committing to accepting payment for cross border trade in currencies other than the dollar, despite US insistence that the only currency for pricing commodities, settling international trade, and therefore the reserve currency must be its own.

We also know that since the Second World War, the US Government has acted robustly against dissenters to enforce its currency monopoly. Libya’s Ghaddafi and Iraq’s Saddam Hussein both proposed new currencies to free themselves from the dollar and came to a sticky end. But all monopolies eventually fail. Encouraged by signs that the dollar’s has now run its course, increasing numbers of nations are abandoning it.

When the US was the world’s policeman, very few countries would have dared to challenge the mighty dollar. American foreign policy was driven by its battle against communism, protecting economic freedom for nations in its sphere of influence. But for the ruling elites around the world, America created distrust and resentment. These are the world policeman’s legacy.

A seminal event, which westerners have mostly forgotten about, was the Asian crisis of 1998. China believes it was planned by the Americans for their own benefit. Here is an extract from an important speech by Major General Qiao Liang, strategist for the Peoples’ Liberation Army, to the Chinese Communist Party’s Central Committee in April 2016, when he laid down what has become China’s version of events:

“What was the hottest investment concept in 1980s? It was the “Asian Tigers.” Many people thought it was due to Asians’ hard work and how smart they were. Actually, the big reason was the ample investment of U.S. dollars.

“When the Asian economy started to prosper, the Americans felt it was time to harvest. Thus, in 1997, after ten years of a weak dollar, the Americans reduced the money supply to Asia and created a strong dollar. Many Asian companies and industries faced an insufficient money supply. The area showed signs of being on the verge of a recession and a financial crisis.

Don’t wait for a stock market crash, dedollarization, or CBDCs before securing your retirement with physical precious metals. Genesis Gold Group can help.

“A last straw was needed to break the camel’s back. What was that straw? It was a regional crisis. Should there be a war like the Argentines had? Not necessarily. War is not the only way to create a regional crisis.

“Thus, we saw that a financial investor called “Soros” took his Quantum Fund, as well as over one hundred other hedge funds in the world, and started a wolf attack on Asia’s weakest economy, Thailand. They attacked Thailand’s currency Thai Baht for a week. This created the Baht crisis. Then it spread south to Malaysia, Singapore, Indonesia, and the Philippines. Then it moved north to Taiwan, Hong Kong, Japan, South Korea, and even Russia. Thus, the East Asia financial crisis fully exploded.

“The camel fell to the ground. The world’s investors concluded that the Asian investment environment had gone south and withdrew their money. The U.S. Federal Reserve promptly blew the horn and increased the dollar’s interest rate. The capital coming out of Asia flew to the U.S.’s three big markets, creating the second big bull market in the U.S.

“When the Americans made ample money, they followed the same approach they did in Latin America: they took the money that they made from the Asian financial crisis back to Asia to buy Asia’s good assets which, by then, were at their bottom price. The Asian economy had no capacity to fight back.

“The only lucky survivor in this crisis was China.”

Whether Qiao was right in his assessment is not the point: this is what the Chinese leadership believes. And in early 2014, they became aware of US plans to stoke up dissent in Hong Kong, which led to student riots later that year. While America has tried several times to provoke China since then (trade tariffs, technology bans, the Huawei saga, Taiwan…), the only action China has taken is to defensively impose greater control over Hong Kong which was demonstrated by American action to be her weak point.

Finally, China’s patience over the dollar appears to be paying off. It has not interfered with America’s global plans, beyond ensuring with Russia that the Asian continent is their joint fiefdom.

But China’s economic tentacles are not confined to Asia. It trades everywhere, and its business and investment plans offer better prospects for all Africa, South America, and even Mexico. If it wasn’t for fear of American reprisals, their support for China and willingness to take its currency in payment would have already happened. But then America took a step too far in sanctioning Russia and leaning on Brussels-based SWIFT to cut Russia out of the dollar-based global payments system.

NATO and the EU fell in line with the Americans, while Asia, numerically far larger in population, backed Russia. The Americans had miscalculated, and for Russia it was business almost as normal while the western alliance suffered soaring energy, commodity, and food prices. This triggered rising interest rates and now credit contraction, leading to an initial banking crisis six weeks ago with the failure of Silicon Valley Bank and Credit Suisse in Europe. In the last six months, the dollar’s trade weighted index has fallen 11%.

Not only has America now demonstrated to every non-aligned nation that its dollar’s power is overrated, but by imposing sanctions on Russia it ended up destabilising its own financial system. And now, non-aligned nations have a free choice: stick with America, its dollar, and its discredited financial system, or deepen ties with China with her credible economic plan and whose economy is now growing.

While there is an element of short-termism in this choice, for the longer-term China offers something which America, its World Bank, and regional network cannot. The World Bank dishes out some charity, which allows it to fill its glossy handouts with tales of doing good. But any emerging nation seeking credit gets it in dollars (which it has to repay, thereby maintaining demand for it) and has to satisfy a business-cum-political case for the loan.

Dealing with China is different. Because her commercial interests align with those of her trading partners, China invests in infrastructure directly on its own or in partnership, building railways, highways, and communications. China can afford to do this because she has a savings driven economy. Furthermore, there are two currencies, onshore and offshore keeping offshore credit from migrating onshore. Therefore, the consequences for consumer price inflation of credit expansion are minimised.

Arguably, a shaky banking system is proving to be the dollar’s final undoing. Nations who hesitated before settling trade in renminbi are no longer doing so, understanding that their dollar reserves and balances are now at risk. There is additional safety in their numbers, because there are too many of them to be picked off by America individually. And if the US banking system continues to crumble, the interconnectedness with the other western alliance currencies is also at risk.

Other than those in the American camp, central banks are also re-evaluating their reserve policies. We have seen them add to their gold reserves, which is the same thing as selling dollars. According to the IMF, total foreign reserves fell by the equivalent of one trillion dollars in 2022, with the dollar content alone falling by $600bn. Renminbi in reserves at the year-end were only $298bn equivalent, so presumably they will be added to.

But is there really a need for currency reserves? The only case that can be made is for exchange rate and crisis management. Extending swap lines is inflationary, and a tool deployed only between the six major central banks — the Fed, Bank of Canada, Bank of England, the ECB, Bank of Japan, and the Swiss National Bank. It’s an elite arrangement that excludes the other 149 central banks.

They only need credit liquidity to settle their trade in other currencies. Therefore, a large proportion of dollar reserves held by central banks, which the IMF puts at $6.471 trillion, is becoming available for sale. To this must be added dollars held by private sector actors in the nostro/vostro correspondent banking system.

Don’t just survive — THRIVE! Prepper All-Naturals has freeze-dried steaks for long-term storage. Don’t wait for food shortages to get worse. Stock up today. Use promo code “jdr” at checkout for 25% off!

The end of the petrodollar’s monopoly

In so far as the public is aware, the dollar’s hiatus kicked off last December, when President Biden visited Saudi Arabia, followed by President Xi. The difference in their reception said it all, with Biden accorded a low-key welcome while Xi was honoured with all the Arab pomp and ceremony Muhammad bin Salman could muster. It was at Xi’s meeting that the Saudis agreed to accept payment for oil in renminbi.

These were merely the latest in a long line of developments. In 2014, a director of one of the major Swiss gold refiners told me that they were working round the clock recasting LBMA 400-ounce bars into the new 99.99 Chinese kilo standard. Bars from the Middle East, many of which appeared to have come out of long-term storage, were being returned to their owners recast to the new kilo standard. The only conclusion is that nine years ago the Arab world saw the future for their wealth being bound up more with China and Asia than with the Europeans and Americans. Coincidently, that was when America was believed by China to be stoking up trouble in Hong Kong, and provoking Russia into taking Crimea.

Further confirmation of how the geopolitical plates were shifting came in 2018 when President Putin and MBS high-fived at the G20 conference in Buenos Aires. From their body language it was clear that there was a confidential understanding between the two leaders and that they were working together. And in the five years since, the determination of Europe and North America to ban fossil fuels entirely has confirmed the foresight of the Arabs who nine years ago were recasting their gold bars into the Chinese standard.

By promising to do away with oil and gas on a rapidly shortening timescale, the West has offered the two Asian hegemons an open goal. Russia, Iran, and Saudi Arabia between them have nearly all the cheap cost oil and have a high degree of price control over global energy markets.

You can tell that America has now lost its influence over the Middle East because peace has returned to the region. Saudi Arabia is mending fences with Iran, Assad of Syria is expected to visit Riyadh shortly, Qatar and Bahrain are resuming diplomatic relations, and the first round of Yemeni peace talks have been successfully concluded. But America is not happy. William Burns from the CIA recently flew to Riyadh seeking a meeting with MBS, presumably to see where the CIA stood in the light of developments and to reconnoitre the situation. The nuclear attack submarine USS Florida transited Suez, in support of the Fifth Fleet and is presumed to be on its way into the Gulf.

Clearly, America’s intention is to escalate tensions, with a threat to attack Iran, whose nuclear programme is well advanced as the excuse. But realistically, the Americans are powerless. And if they do decide to attack Iran, they would also make enemies of the entire region — as MBS surely made clear to William Burns.

Other than security matters, the big issue is over currencies. Of course, the Gulf Cooperation Council members will still accept dollars. But America now has a banking crisis, the Fed itself is deeply in negative equity along with the other major central banks, and foreign holders of dollars have too many for future trade conditions.

The alternative is China and renminbi

It was reported this week that China’s GDP grew by 4.5% in the first quarter of this year, headlined by a recovery in consumer spending with retail sales growing by 10.6% in March alone. And while the west’s financial analysts’ attention is usually directed towards consumer activity first and foremost, everyone else knows that China has a savings driven economy, which allows credit to drive industrial investment without consumer prices inflating.

There is an understandable fear that China’s demand for commodities will keep prices high at a time when America and Europe will enter recession on the back of contracting bank credit. Furthermore, there has been a lack of new mine discoveries and capital investment in commodity extraction, suggesting that commodity and energy supplies will remain tight. But as yet, in China statistical evidence that credit is driving capital formation is yet to emerge.

Indeed, the pause in overall capital investment is consistent with China switching its strategic emphasis from its export trade to America and Europe to developing Asian markets. Furthermore, American manufacturers are reassessing their supply chain arrangements in the current geopolitical atmosphere.

But when it comes to choosing currencies, all the non-aligned nations supplying China know that her plans go far beyond domestic manufacturing with an ambition to bring about an industrial revolution throughout Asia. That is in their minds when they contrast receiving payment for exports in dollars to be lodged in the unsafe US banking system, compared with renminbi lodged in a state-guaranteed Chinese bank. And it is also in their minds when they compare the economic prospects for China compared with those of America and its close allies.

Even America’s allies are becoming unsure of their commitment to dollars. France recently accepted payment in renminbi for liquid natural gas. Other members of the European Union are plainly sitting on the fence, aware that to cut themselves off from the largest economy in the world which is growing while America’s is not, is ill-advised.

Don’t wait for a stock market crash, dedollarization, or CBDCs before securing your retirement with physical precious metals. Genesis Gold Group can help.

Furthermore, Europe has direct rail links across the Eurasian continent not just to China, but also to the entire continent. Shortly, they will connect directly to the Indian sub-continent as well, which is now officially the world’s most populous nation. Even the British cannot afford to follow Washington’s lead and restrain trade relations with China.

Trade imbalances are set to increase for America and much of Europe anyway. National accounting identities tell us that in the absence of changes in savings behaviour, a budget deficit leads to a matching trade deficit — the twin deficits syndrome. As contracting bank credit undermines the US economy, the US Government will face declining tax revenues, increasing welfare costs, and soaring borrowing costs.

The deficit on trade will increase in lockstep with the budget deficit— only this time, the balance of payments will almost certainly increase with the trade deficit because foreign exporters are unlikely to retain their dollar payments.

For the US Government and us all, it is likely to become a two-pronged headache. The first is that foreign demand for US Treasuries will not only disappear, but they will turn sellers when the funding requirement is rising.

Secondly, with global trade payments migrating to renminbi and China’s export trade continuing to thrive on filling America’s increasing trade gap, she will be cast as the villain of the peace. And any attempt by the US Government to introduce yet higher trade tariffs and bans on Chinese technology will not remedy the situation.

It must be acknowledged that a consequence of China’s economy expanding while America’s slumps could turn America’s current sabre-rattling over Taiwan into outright conflict.

Assessing the impact of dollar liquidation

There are two elements of dollar liquidation to consider, commencing with liquid bank deposits, certificates of deposit, Treasury, and commercial bills etc. with maturities of less than one year. According to the US’s Treasury International Capital statistics, at end-December these amounted to $7,074bn in credit liabilities due to all foreigners. This is the immediate amount that potentially hangs over foreign exchange markets.

At the same time, US residents have liabilities to them in foreign currencies of the equivalent of only $384bn. The ratio of foreign owned dollars to US owned foreign currency is 18.4 times. Put another way, this is the approximate imbalance between potential dollar selling by all foreigners and the ability of US buyers to absorb it by selling their foreign currency in return for dollars. On the face of it, this differential could fuel a rapid fall in the dollar’s exchange rate against foreign currencies.

It is also possible that a bank will buy in dollars for its own book and creates credit in a foreign currency in favour of the dollar seller. But that activity is likely to be limited to branches of foreign banks in New York with access to the relevant foreign wholesale credit markets and assumes they would wish to buy dollars.

But the most likely method to stop a sliding dollar would be either for the exchange stabilisation fund to intervene, which would reduce broad money supply when the Fed would be struggling to stop it contracting further; or for the Fed to seek cooperation from its swap line partners to buy dollars and sell their own currencies in return, which is highly inflationary.

This leads us to consider the outlook for interest rates and how foreign perceptions of financial risks might change, particularly with regard to systemic risk in the US banking system. We know that a weakening currency tends to lead to higher interest rates. And that rising interest rates might be expected to support the dollar’s exchange rate.

But there is the danger of a negative feed-back loop, whereby risks to the dollar’s exchange rate increases along with interest rates. This is because rising interest rates will destabilise the US economy and government finances, leading to higher budget and trade deficits. And portfolio assets, defined as being of more than one year’s maturity will fall in value.

Subscribe for free to the America First Report newsletter.

The chart above shows how foreign holdings of long-term securities have been inflating in recent years on a quarter-to-quarter basis, mainly due to an increase in foreign private holdings. In January, private and public sector holdings totalled $24,548bn. And though choppy, there now appears to be a declining trend. These figures are in addition to foreign owned non-financial assets, such as real estate, farmland, factories, and offices.

US ownership of foreign long-term securities totals $14.263 trillion, of which $10,875bn is in corporate stocks. It should be noted that in the majority of cases, foreign securities are held in dollar-priced American Depository Receipts (ADRs), so that their disposal does not result in foreign exchange transactions, unlike a foreign disposal of a dollar-based asset which does.

But commercial bank credit in major jurisdictions has stopped growing or is even contracting while demand for credit continues to increase. The consequence is that interest rates will continue to rise, due to this imbalance of supply over demand. There is little that central banks can do about it without debasing their currencies.

And because they are under pressure to ensure the funding of their governments’ increasing deficits, they will be forced to accept the market’s pricing of credit. That was the experience of the 1970s.

While everyone’s attention is being misdirected to forecasts of CPI inflation, they appear to be unaware that inflation is not the immediate issue. It is the shortage of bank credit, which is now driving interest rates, not inflation expectations. Accordingly, the outlook is for yet higher bond yields which means that all financial asset values will fall further.

And as they fall, the highly financialised US banking system will be undermined by both investments held on their balance sheet and by collateral held against loans. But this outlook is not confined to dollar markets and is shared by all other western financial centres. As these dynamics become obvious to investors, a global liquidation of financial assets is bound to accelerate, with the exception perhaps of China’s financial markets which are set on a completely different course, and Russia’s which have been completely cut off from global investment flows.

In a general portfolio liquidation, the imbalance between foreign investment in long-term assets and the US ownership of foreign investments will drive relative currency outcomes. In dollars, it is a ratio of $24,548bn to $14,263bn, or approximately 1.72 times. But for foreign exchange purposes, probably less than a trillion dollars are being held denominated in foreign currencies, with the balance in ADRs.

When an ADR is sold, there is no foreign exchange transaction involved, unlike selling of foreign owned US securities. Therefore, a general portfolio liquidation would see an overwhelming excess of dollar selling by foreigners compared with foreign currency liquidation by Americans.

Assuming that foreign holders reduce their dollar exposure and at the margin buy renminbi, the fall in the dollar relative to the renminbi could be unexpectedly sudden and substantial. At least some of the dollar liquidation is likely to fuel energy and commodity prices, whose supply is in many cases too limited to support stockpiling on any scale.

Gold which is likely to be bought because it is still legal money in nearly all foreign jurisdictions. It would mark a foreigner-driven flight out of unanchored credit into physical commodities due to increasing counterparty risk.

The only offset to these negative implications for the dollar’s future is likely to come from other members of the western alliance. As major foreign holders of US Government debt, they can be relied upon to attempt mutual currency support. Doubtless, the Fed and its five partner central banks will increase their swaps to that end as well as to shore up the dollar itself.

But these actors are in the minority measured by the quantities of dollars held, and their attempts to rig foreign exchange markets will only make things worse.

- Concerned about your life’s savings as the multiple challenges decimate retirement accounts? You’re not alone. Find out how Genesis Precious Metals can help you secure your wealth with a proper self-directed IRA backed by physical precious metals.

We must therefore conclude that with the evidence pointing to foreign selling of the dollar, that this selling could quickly escalate. Consequently, dollar liquidation by foreigners will lead to significantly higher interest rates which can only be lessened by the expansion of central bank credit.

And that expansion can only come from the Fed because commercial banks are tapped out, seeking to contain their losses and reduce their balance sheet leverage. And if the Fed resorts to the printing press through currency swaps or by other means, the dollar will have had it anyway.

Russia’s position

The Russian economy appears to be doing remarkably well during the current conflict with Ukraine. Taxation and government debt are lower than in any other major economy, and with a few workarounds, the export trade continues in surplus. The conflict in Ukraine has been a financial burden, but not enough to destabilise Russia’s economy.

Payment flows have been diverted from dollars into Chinese yuan, permitting Russian ex-pats around the world to continue to use their credit cards. And Bangladesh has been paying Russia for its Rooppur nuclear power plant construction in yuan via a Chinese bank with access to China’s cross-border interbank payment system. As we have seen so many times in previous cases, sanctions against Russia are proving to be utterly pointless.

While the yuan payments route deals with the current situation, we can be sure that Russia will want to have a payment medium under its own control. It is to that end that on Putin’s behalf Sergey Glazyev is working on a proposal for a new trade settlement currency for the Eurasian Economic Union. The indications are that it will be based on gold, and it is likely from what Glazyev has publicly written that the rouble will move onto a gold standard of sorts as well.

The immediate benefit to Russia’s business community is that current interest rates of over 10% will fall substantially. It compares with a consumer price inflation rate of 3.5%, but that is heavily distorted by previously high CPI inflation rates. Nevertheless, anything that reduces interest rates in this lower inflation environment will encourage the growth in credit to maximise economic potential.

The key to it is for the value of credit to be anchored to gold to introduce permanent price stability. Only then can rouble interest rates decline to a few per cent permanently.

The rouble would then be in a position to challenge a fiat yuan as a payment medium. And with Russia’s new relationship with the Gulf Cooperation Council members, no doubt a gold-backed rouble would be readily accepted by the Saudis and others for energy payments, even in preference to yuan.

The negotiations between Russia and China on this point are likely to be tricky. But given that we know China has massive undeclared gold stocks anyway, talks can be resolved in the interests of a stable monetary relationship between the two hegemons. Of more importance perhaps, is the question of at what gold value the rouble will be exchangeable for notionally or actually, given that Putin’s unfriendlies face a financial, banking, and fiat currency crisis likely to drive fiat values for gold considerably higher as they rapidly lose purchasing power.

Read the full article at Goldmoney.com, cross-posted from Medical Kidnap.

It’s becoming increasingly clear that fiat currencies across the globe, including the U.S. Dollar, are under attack. Paper money is losing its value, translating into insane inflation and less value in our life’s savings.

Genesis Gold Group believes physical precious metals are an amazing option for those seeking to move their wealth or retirement to higher ground. Whether Central Bank Digital Currencies replace current fiat currencies or not, precious metals are poised to retain or even increase in value. This is why central banks and mega-asset managers like BlackRock are moving much of their holdings to precious metals.

As a Christian company, Genesis Gold Group has maintained a perfect 5 out of 5 rating with the Better Business Bureau. Their faith-driven values allow them to help Americans protect their life’s savings without the gimmicks used by most precious metals companies. Reach out to them today to see how they can streamline the rollover or transfer of your current and previous retirement accounts.