Since its founding in 1913, the unelected central planning bureaucrats at the Federal Reserve have been given the incredible privilege of legally creating money out of thin air, which mere mortals like us are not allowed to do. They have also been given the tremendous responsibility of maintaining (1) maximum employment, (2) a stable price level, and (3) low interest rates.

How have they done so far?

Since 1913, the bureaucrats at the Fed have helped cause

- over 20 percent price inflation by printing money for World War I

- the depression in the early 1920s, with over 15 percent price deflation

- the Great Depression of the 1930s, with 25 percent unemployment and over a 10 percent collapse in the gross domestic product (GDP) of the United States

- the “stagflation” of the 1970s, with double-digit inflation and interest rates

- the housing bubble in the first decade of the twenty-first century

- the Great Recession of 2008–9

- a 40 percent increase in the money supply in response to covid

- aggressive interest rate hikes over the past year, which will likely cause the twenty-first recession since the Fed was founded

Of course, there were boom-and-bust business cycles before the Fed was created, due to government laws allowing fractional reserve banks to create money out of thin air, as well as various government interventions in money and banking.

However, we are told the Fed was created to help smooth out the business cycle and create a more stable and prosperous economy.

Below, I review some key economic data before and after the Fed was created to see five important ways the Fed has made the economy worse than it would have been otherwise.

Unemployment Became Much Higher

Unfortunately, unemployment data is not available for most of the nineteenth century, but what data is available shows that unemployment was generally very low since everyone who wanted to work could get a job if they were willing to accept market wages.

There were typically no legal restrictions then that prohibited voluntary work transactions. Thus, wages were allowed to fluctuate according to supply and demand, just like any other price on the free market, which generally led to full employment.

The chart below shows US unemployment rates from 1890 to 1988. The key takeaway is that before the Fed was created, unemployment never reached the incredibly high levels seen during the Great Depression of the 1930s, which occurred more than seventeen years after the Fed was created to “smooth out” the business cycle. Let’s also not forget that unemployment rose to 10 percent or more during the Great Recession of 2008–9 and the covid panic of 2020.

Figure 1: Unemployed workers and unemployment rate, United States, 1890–1988

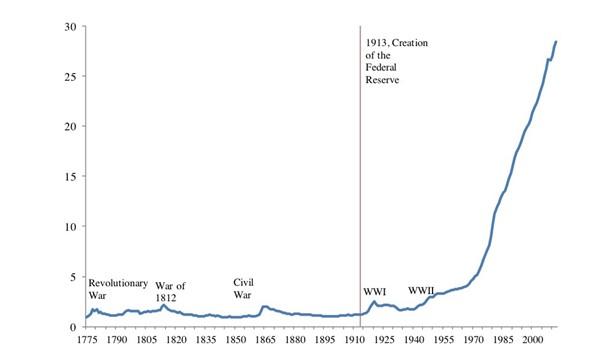

Inflation Has Been Much Higher

Inflation is where the Fed’s track record of failure is most obvious.

The chart below shows the US Consumer Price Index of inflation from 1775 to 2012. Outside of brief inflationary spikes driven by money printing to fund wars, inflation was virtually nonexistent prior to the creation of the Fed in 1913. Since then, inflation has skyrocketed, particularly after all ties between the US dollar and gold were severed in 1971. As a result of this inflation due to Fed money creation, the dollar has lost 97 percent of its value since 1913.

Figure 2: Consumer Price Index, United States, 1775–2012 (level, 1775 = 1)

Interest Rates Became Much Higher

The chart below shows US long-term interest rates from 1790 to 2011. While interest rates have always been volatile before the Fed, they never reached the all-time high levels they reached in the early 1980s. Those high interest rates were the market’s reaction to the double-digit inflation of the 1970s caused by the Fed’s aggressive money creation.

Figure 3: Long-term interest rates, United States, 1790–2011

Economic Growth Has Been Slower

While it is hard to compare the economy in different centuries, the fact is that economic growth was higher before the Fed was created than after. The chart below shows real GDP growth from 1800 to 2020. Growth was higher from 1800 until the Fed was created in 1913, as shown by the steeper slope of real GDP growth before 1913 as compared to after 1913.

Figure 4: Real GDP in 2012 dollars, United States, 1800–2020

During this time of unprecedented economic freedom (except for the obvious evils of slavery) and minimal taxation, the US went from being an economic backwater to perhaps the wealthiest country in the history of the world by 1913.

While other government economic interventions and taxation have contributed to slower growth since 1913, the Fed shares a good deal of the blame. The Fed contributes to slower economic growth by helping cause the boom-and-bust business cycle, which causes the waste of scarce resources on bad investments, lowering worker productivity and real wage growth below what it would have been otherwise.

Government Deficits and Debt Have Skyrocketed

By creating money out of thin air to buy the US government’s debt, the Fed enables the federal government to spend much more than it takes in with taxes.

The charts below show US government deficits and debt as a percentage of GDP since 1857. Prior to the Fed’s creation in 1913, sizable budget deficits only occurred during wars such as the Civil War. There were budget surpluses (yes, surpluses!) in most of the other years.

However, since the Fed was created, budget deficits have been the rule, reaching as high as 30 percent of GDP during World War II and 15 percent during the covid panic. Deficits are currently 5.4 percent of GDP. Before 1913, that level was only exceeded during the Civil War.

As a result of all this deficit spending, US debt to GDP has skyrocketed since the Fed was created. Debt to GDP rose to 30 percent during the Civil War, before falling back toward 0 percent before World War I. It has been over 30 percent for most of the years since 1913, even exceeding 112 percent during World War II. Publicly held debt to GDP is currently at 93 percent and rising.

Figure 5: US government budget deficits and surpluses as well as debt held by the public (percentage of GDP), 1857–2023 and projections to 2053

Conclusion

Along with the Soviet Union, the Fed has proven that central planning of the economy by a small group of government bureaucrats does not work.

The fact is that the Fed was not created to help the economy. It was created by bankers to help fractional reserve banks create even more money out of thin air and bail them out when they get in trouble.

Money and interest rates are the lifeblood of our economic system, and they provide key signals for consumers and businesses. By constantly manipulating both the money supply and interest rates in the belief that they know more than millions of people, the Fed creates tremendous economic instability, which wastes scarce resources and lowers living standards, particularly for the poorest among us.

Money is just a medium of exchange to make life easier and more productive than barter. The supply of money we have now gets that job done. There is no need to change the money supply.

With 100 percent bank reserves, we would not have to worry about bank runs, a decline in the money supply like in the 1930s, inflation, and the boom-and-bust business cycle. We also wouldn’t need government bureaucrats like Jay Powell pretending they can centrally plan the economy.

If the economy were ever set free of the constant money and interest rate manipulation of the Fed and fractional reserve banks, it would lead to unprecedented economic stability and prosperity.

About the Author

Jon Wolfenbarger is Founder and CEO of Bull And Bear Profits, an investment website. Send him email. Article cross-posted from Mises.

Let’s just drop all the parsing and keep it simple:

LAEL BRAINARD, the vice chairperson of the Fed is a WEF member and pro–CCP!

Got it????

(Yet not a single mention of this in this article???? Frigging ever wonder why???)